DIGITAL READINESS

HOW DIGITALLY READY

ARE THE URBAN ULTRA-POOR?

Urban slums and low-income residential communities represent dense, self-contained transaction ecosystems that are relevant targets for digital payment and finance programs.

Urban slums and low-income residential communities represent dense, self-contained transaction ecosystems that are relevant targets for digital payment and finance programs. Financial inclusion through digitization of the payment landscape can ensure direct and tangible benefits in the form of reduced volatility in household income and expenditure as well as overall financial stability.

IFMR LEAD and Catalyst, in collaboration with SEWA Bharat, conducted a survey of 442 ultra-poor households in the Bhatta Basti area of Jaipur which has a largely migrant settlement of approximately 10,000 households with an estimated population over 45,000 persons.

The survey focused on documenting the current needs, behaviors, and perceptions with regard to digital payments and finance.

DIGITAL READINESS QUALIFIERS

WHAT DOES THE URBAN ULTRA-POOR LOOK LIKE?

BANK ACCOUNT OWNERSHIP AND USAGE

MOBILE OWNERSHIP AND USAGE

Smartphone Usage

AWARENESS AND PERCEPTIONS ON DIGITAL PAYMENTS

HOUSEHOLD PREFERENCES REGARDING MODE OF PAYMENTS ARE INFLUENCED BY THEIR KNOWLEDGE, ACCESS AND WILLINGNESS

While cash is still the most preferred choice for making payments on most dimensions, the community sees merit in digital from greater security and proof of record.

Difficulty with usage and understanding

Merchant preferences for cash-based payments

Lack of access to digital money solutions

WHAT DO WE KNOW?

The needs assessment study recorded that the ultra-poor migrant community of Bhatta Basti, although interested in trying digital payment systems, does not yet have the technical and logistical capabiities needed to do so wholly and immediately.

Key ecosystem actors including financial service providers, local government agencies, and enablers like Catalyst or local community organizations need to collaborate so that systematic efforts can be put in place to ensure active banking, greater access to internet and payment devices, and higher awareness regarding non-smartphone based payments like USSD and AEPS.

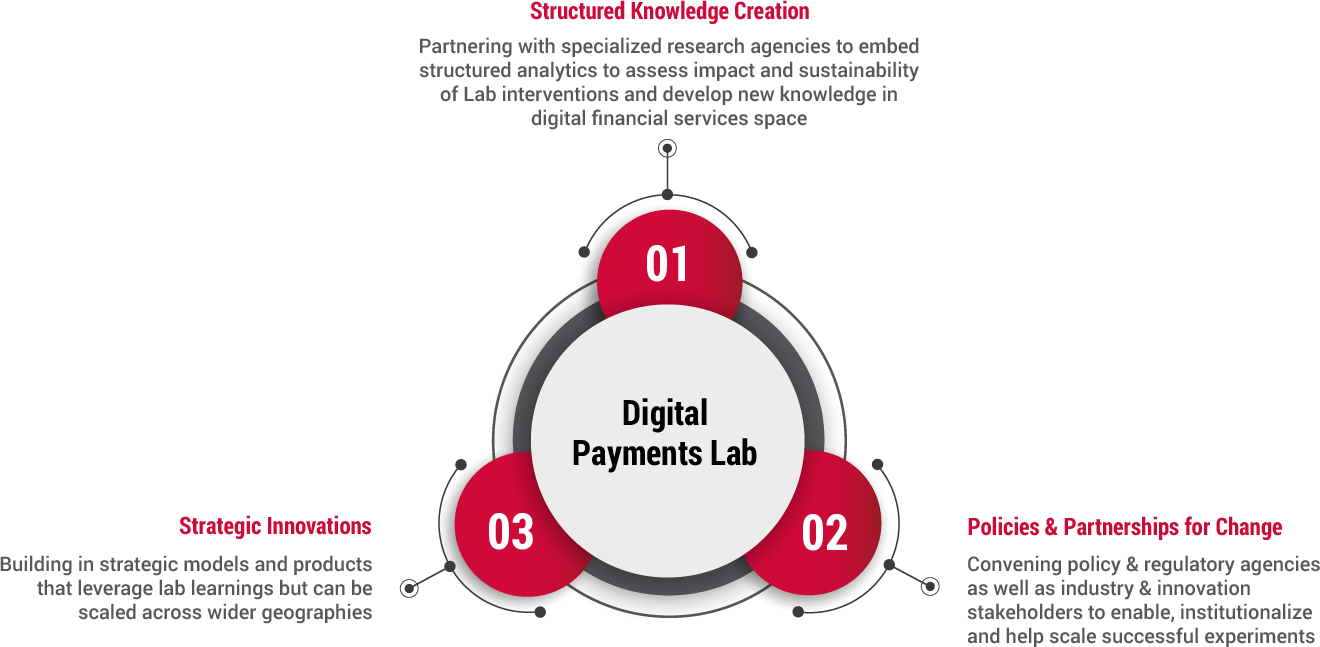

WHAT CAN BE DONE?

A staged, structured approach to the above is needed to improve digital payments and finance penetration in the community. This will require a multi-stakeholder effort comprised of Financial Service Providers, Government Agencies, Community Organizations and change ‘Enablers’ such as Catalysts.